If your tax strategy begins in March, you have already missed the real opportunities.

If your tax strategy begins in March, you have already missed the real opportunities.

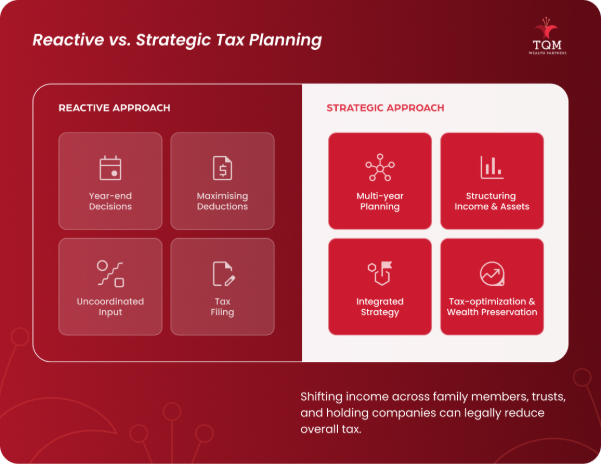

For most taxpayers, tax planning is just filing in the tax season.

But for wealthy individuals, it’s about making decisions throughout the year.

Most high-income individuals don’t overpay taxes because of income; they overpay because of poor structure.

The real opportunities? Wealthy individuals don’t see taxes as just a compliance task but as a year-round strategy. They think of it as a system. They embed tax planning strategies into estate structures, business decisions, and investments, reducing their tax burden by 15–30%.

In our experience working with high-income individuals, the largest tax inefficiencies don’t come from lack of knowledge; they come from the absence of coordination across financial decisions.

If you want to understand how this works in practice, start with a year-round tax planning approach.

What Are Tax Planning Strategies?

Tax planning strategies are simple, coordinated, and legal ways to reduce tax liability by managing investments, income, and financial timing efficiently.

Tax filing is a backward-looking exercise, while tax planning is forward-looking, typically designed 12 months to even several years in advance.

1. They Control When Income Is Taxed

Most taxpayers think in terms of income. Wealthy individuals focus on income timing.

This is a subtle but powerful shift.

Common approaches:

- Strategically delaying business income or bonuses to the next tax year.

- One common strategy involves shifting income into retirement accounts to prevent income recognition.

- Controlling when equity compensation is realized to reduce tax exposure.

Example:

Deferring $60K of income into the next tax year, a business owner lowers the taxes at marginal rates, saving up to 15% in a single move.

We’ve worked with affluent clients in the $500K-$10M income range effectively, lowering their effective tax exposure simply by deferring income across tax years and avoiding tax leakage.

This is one of the straightforward yet most overlookedtax planning strategies.

2. They Shift IncomeintoLower-Tax Entities

Most high earners structure income beyond their personal names.

Instead, they spread income across:

- Family members in lower tax brackets

- Trusts

- Holding companies

This significantly reduces the overall tax burden legally.

Why it works:

The US tax system operates under a progressive tax structure, where allocation across entities and /or individuals can lower the tax rate significantly.

3. They Maximize Tax-Advantaged Investments

Wealthy individuals care less about returns; they prioritize after-tax outcomes.

Popular vehicles include:

- Retirement accounts (401(k), IRA)

- Municipal bonds (tax-free interest in the U.S.)

- Insurance-linked investment products

- Equity investments held long-term for capital gains benefits

Learn how the IRS outlines these accounts to be a valuable tool for tax saving:

Key insight:

In practice, two portfolios with similar outcomes can exhibit different after-tax outcomes.

To dig deeper into the issue, explore a comprehensive financial plan:

4. They Harvest Losses (On Purpose)

Yes, wealthy investors take loss-making decisions on purpose.

It is called the tax-loss harvesting strategy.

How it works:

- Exiting underperforming assets to capture tax losses

- Using those losses to offset capital gains

- Reduce total taxable income

The IRS highlights the rules around this strategy.

Example:

If you gain $100K but make $40K in losses, it reduces taxable gains to just $60K.

This strategy is designed to optimize after-tax portfolio outcomes.

We regularly see portfolios where strategic loss harvesting offsets a significant portion of annual gains, particularly in volatile markets

5. They Use Deductions Strategically (Not Randomly)

Most taxpayers look for deductions at tax time. Wealthy individuals incorporate them into their financial plan.

Strategic deductions include:

- Optimizing expense categorization to maximize allowable deductions.

- Leveraging depreciation to reduce overall tax exposure.

- Using donor-advised funds to make charitable contributions to reduce tax load.

- Offsetting interest costs from leveraged investments.

Example:

A wealthy individual who invests in real estate offsets rental income through depreciation, reducing taxable income significantly.

6. They Plan for Inheritance Early

One of the largest tax exposures takes place during intergenerational wealth transfer.

In the absence of a structured plan, estates may be exposed to significant tax erosion.

Common strategies:

- Spreading out gifts to stay within the tax-free limits.

- Using trusts to simplify and optimize wealth transfer.

- Creating liquidity through insurance to avoid forced asset liquidation.

- Utilizing valuation discounts to conservatively minimize taxes

Refer to official IRS guidelines on estate and gift tax limits

Example:

Families that begin estate planning 10-15 years in advance can significantly lower the tax exposure as compared to reactive planning.

7. They Align Business StructurewithTax Efficiency

Many entrepreneurs often overpay taxes, not because they earn more, but because of poor financial structuring.

Wealthy business owners optimize:

- Salary vs. dividend mix

- Corporate vs. personal taxation

- Expense allocation

- Cross-border structuring (if applicable)

Example:

Choosing the right entity structure (S-corp vs. C-corp) can significantly reduce tax liability.

8. They Work with Coordinated Advisors

Here’s where most high earners go wrong:

Even with a great team in place, you can end up paying more taxes through the cracks in your current strategy

This is because no one is aligned.

According to industry estimates, a significant portion of affluent individuals operate without an integrated financial structure, leading to missed optimization opportunities.

This often increases the overall tax burden as a result of overlapping strategies, suboptimal timing of income and gains, and missed deductions.

Most wealthy individuals don’t rely on isolated strategies; instead, they use a structured, coordinated approach.

9. They Think in Multi-Year Horizons

Tax efficiency isn’t achieved in a year; it is achieved over time.

This process includes:

- Planning sales of large assets.

- Preparing for major liquidity events like a business exit before they occur.

- Long-term planning of gain realization.

- Managing retirement income withdrawals with precision.

Additional strategies often include asset location optimization, tax-loss harvesting, and income deferral techniques to spread tax liabilities across years.

Example:

Exiting a business in phases instead of a single event can lower the tax liability significantly.

According to industry studies, proactive tax planning and coordinated financial strategies can improve after-tax returns by 1–2% annually, which compounds significantly over time for high-net-worth portfolios.

The Real Takeaway

Tax efficiency isn’t about tactics; it’s about structure, coordination, and planning.

Most people:

- Think about filing in March. a

- They are concerned about deductions, not gains.

- They have a fragmented approach.

Wealthy individuals:

- Don’t react at tax season; they plan it in advance

- Control when income is realized to lower tax exposure.

- Invest at the right time for maximum tax reduction.

- Make sure their advisors are on the same page.

Common Mistakes That Increase Taxes for High Earners

Even wealthy individuals with steady income overpay taxes because of the absence of a structured financial plan.

The most common mistakes:

- Treating tax planning as a compliance rather than a strategy

- Working with multiple advisors without a unified strategy

- Ignoring asset allocation when building a portfolio strategy

- Avoid generational wealth transfer planning until it’s too late

As per industry research, holding tax-inefficient investments in taxable accounts increases unnecessary tax drag.

Insight:

Most tax inefficiencies aren’t caused by a single bad decision but small, repeated, and misaligned decisions over time.

These gaps compound over time and often go unnoticed until they impact long-term wealth substantially.

What to Do Next

If you want to make your tax planning effective:

- Start planning in advance, at least 6–12 months ahead.

- Review income composition along with expenses.

- Ensure investment strategy reflects tax implications.

- Explore professional financial planning services

Bring investments, estate planning, and tax strategy under a single coordinated framework.

Structure income sources proactively to improve after-tax outcomes.

Final Thought

Quick question:

If your income increases by 30% next year, would you consider simply paying more taxes, or might you explore adjusting your financial strategy?

For wealthy individuals, without a structured tax plan, increased income often leads to leakage, not progress.

From what we’ve observed, tax inefficiency is rarely dramatic; it’s the accumulation of small, uncoordinated decisions over time.